News

California Fiscal Issues and Information page

California Fiscal Focus

Summary Analysis of General Fund Cash Receipts (2007 - 2014)

October 2013 Cash Report Summary Analysis

More on California Fiscal Policy: How Income Tax Withholding Affects Borrowing Patterns

News

California Fiscal Issues and Information page

California Fiscal Focus

Summary Analysis of General Fund Cash Receipts (2007 - 2014)

October 2013 Cash Report Summary Analysis

More on California Fiscal Policy: How Income Tax Withholding Affects Borrowing Patterns

More on California Fiscal Policy: How Income Tax Withholding Affects Borrowing Patterns

Published October 10, 2013

Recent revenue reports have shown that the collection of General Fund revenues tend to accelerate over the fiscal year, so that more revenue flows to the State in the latter half of the year. One reason for this collection delay is attributable to the unique administrative nature of the State’s largest revenue source, the personal income tax.

The State’s trend of expenditures exceeding revenues in the first few months of the year is nothing new. For 30 of the past 31 years, the State has used short-term external borrowing (known as Revenue Anticipation Notes or RANs) to smooth over cash shortages in the fiscal year.

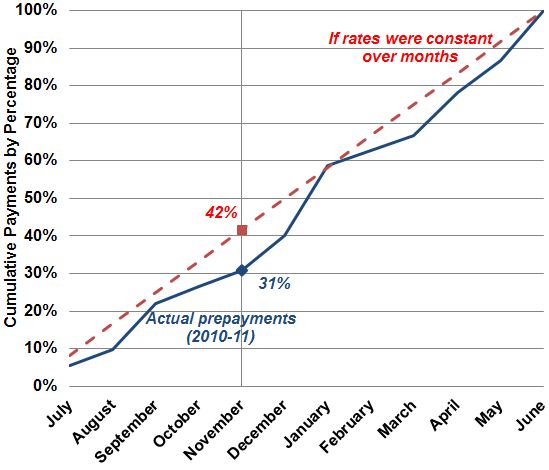

State and federal law require that certain (typically high-income) taxpayers make prepayments on their estimated tax liabilities throughout the year. Data from the Franchise Tax Board seem to suggest that payment practices are not uniform across the months. To illustrate, Figure 2 graphs the payments made in 2010-11. It shows that for the first five months of the year, taxpayers submitted payments totaling about a third of their annual payments. As graphed in the blue line —which marks actual cumulative payments made for the year —rates accelerated in December and January.

The figure’s red line shows how collections would progress if taxpayers made equal monthly payments over the course of the year. When the blue line is below the red line, it can be said that payments are lagging a uniform rate. For February through May, withholding also lags, but actual payments catch up in June.

If 2010-11 is a typical pattern, it can be seen that payment patterns contribute to the state’s intra-year borrowing needs.

Figure 2: A Comparison of Prepayment Patterns

Actual Payments by Month (2010-11) and Assuming Payments Are Made on a Uniform Basis over the 12 Months

Source: FTB MIS Report & WSCS Revenue Report, 5/2/12